Nigel Headford – CAB Chief Executive

UK construction output is predicted to decrease by 2.9% in 2024, followed by a rebound of 2.0% in 2025. This forecast is slightly more pessimistic than what was anticipated three months ago. The downward revision in the projections is mainly attributed to the delay in recovery of the private housing new build and repair, maintenance, and improvement (rm&i) sectors, which are the two largest in construction. This delay is a result of weakened demand and sentiment in the overall housing market since Easter, following the rise in mortgage rates.

Compiled in conjunction with the CPA (the Construction Products Association) the CAB State of Trade Survey is completed alongside the Summer 2024 edition of the CPA’s Construction Industry Forecast.

Unusually CAB Members ‘Historic Sales Volumes’ were below anticipated for Q2, reporting -15% on net balance compared to the wider construction products market which reported an increase of 30% on net balance from respondents. It is unclear why the CAB Membership fared worse in Q2 as in previous quarters the Membership reported more positively. The slowing of the market could be attributed partly due to the very poor weather experienced year to date. With a positive Q2 from the overall Construction products market it is anticipated that this will pull through into a positive position for Members in Q3.

‘Expected Sales Volumes’ for Q3 have softened considerably since Q2 indicating a cautious outlook ahead at the timing of the Q2 survey. Members ‘Expected Sales Volumes’ dropped from 62% on net balance for Q1 to just 20% of Members on net balance in Q2. Now that there is a change of government which has a very positive forecast for the next few years, especially in the new house build market, it is anticipated this will lead through to revitalised output expectations in Q3.

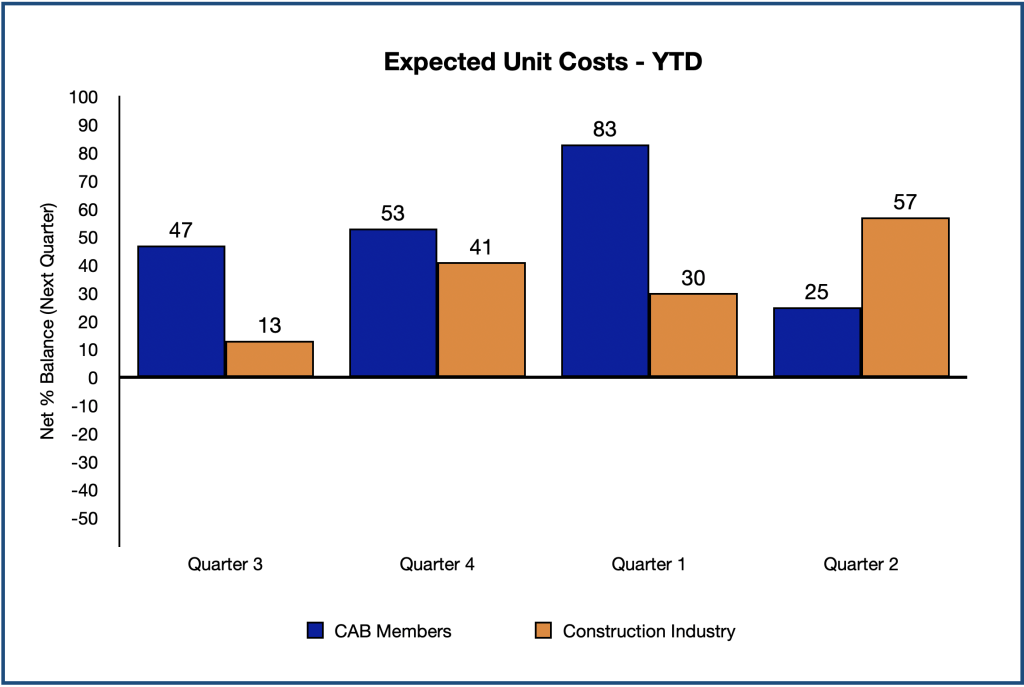

Whilst rising material and labour costs continue to feed through into the construction products market the pressure on costs have decreased slightly in Q2 on net balance of Members. ‘Historic Unit Costs’ have reduced from 60% to 40% in Q2. ‘Expected Unit Costs’ forecasted by Members has reduced considerably from 83% to 25% on net balance of Members. It is suggested that the continued stability of aluminium costs based on supply availability is helping to keep unit costs under control. This anticipated stability, however, is in stark contrast to the wider construction products supply which are anticipating an increase pressure in unit costs in 2024.

Members actual ‘Sales Volumes’, both ‘Quarter on Quarter’ and ‘Year on Year’, continue to show a slight decline, however, a greater proportion of members are now reporting less change in Sales Volumes, up to 45% of respondents compared to just 11% ‘Year on Year’ which suggests that the fenestration market continues to stabilise.

Cost Factors for the Membership show a slight softening over the last year on Wages & Salaries, 70% of Members reporting on net balance in Q2 compared to a high of 93% on Members in the past year.

Members continue to report that the ‘Likely Constraints on Activity Over the Next 12 Months’ remains anticipated demand, however, this has softened slightly in Q2 reported by 70% of respondents compared to a high in Q3 2023 of 89% of Members.

The pressure on ‘Labour Costs’ has softened very slightly, both for the last year and anticipated for the year ahead. ‘Labour Force’ availability has also has also softened and 15% on net balance for the last year report a reduction in labour force.

Members report that exports continue to reduce with both ‘Historic Exports’ and ‘Expected Future Exports’ both reducing on net balance of respondents. The number of Members now reporting that they do not export any products stands at 70% of respondents, this is an increase from 12 months ago where 47% of members were reporting that they were exporting products.

‘Capital Investment’ across most sectors of Members businesses is now increasing as opposed to decreasing as reported a year ago, with ‘Plant Improvement’ being the largest investment. Apart from investment in property Members are reporting an increased investment for the year ahead reflecting a cautious, optimistic view for future business in the UK.

It is important to recognise that an Association belongs to its Members and the more influence that Members can bring into the Association, the further it will grow. The CAB Board of Directors is committed to grow the Association and continue to increase value for membership. Should you wish to learn more about the use of Aluminium used in Construction, please contact CAB, join the Association and be recognised as being involved in supporting your Industry and helping to shape its future. More information on our website at c-a-b.org.uk