By Phil Slinger – CAB CEO

Despite the recent IMF report stating that the ‘UK is expected to be only major economy to shrink in 2023’, construction overall seems to be turning as CAB Members are reporting growth in demand for aluminium fenestration and facades.

On a quarterly basis the wider construction supply chain this month, on net balance, now report that just 7% of respondents claim that Historic Sales Volumes are lower than the past quarter, this compares to 20% of respondents claiming that historic sales volumes are lower in the previous Q4 report. CAB members continue to show Historic Sales Volumes on net balance increases for this quarter slightly higher at 38% compared to 35% in the last quarter.

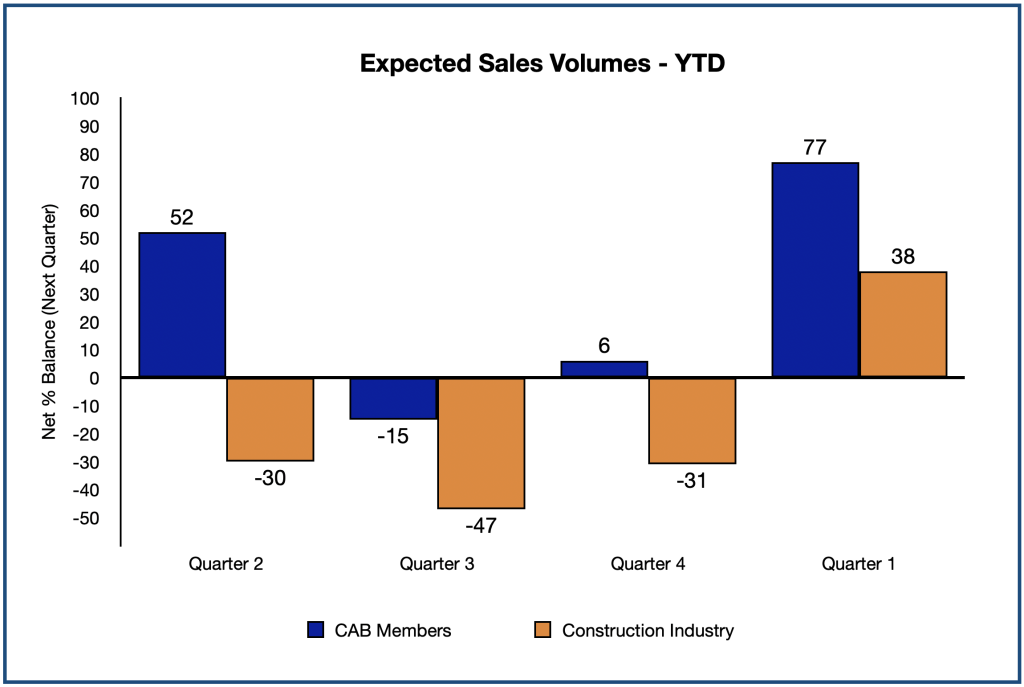

Expected Sales Volumes are the most optimistic for CAB Members for the year with 77% on net balance expecting increases in sales volumes in the next quarter, this is up significantly from the previous quarter where CAB members reported that just 6% on net balance expected sales volumes to increases. Backing this huge shift in Expected Sales Volumes is the wider construction supply chain, where on net balance now 38% of respondents expect sales increases compared to a reduction in sales volumes in the previous quarters report of -31%.

Sales Volumes – Quarter-on-Quarter for CAB Members shows prominent growth with 38% of the Membership reporting ‘Up by over 5%’ compared the previous quarter. The emphasis on growth is even greater on Sales Volumes – Year-on-Year indicating the fenestration industry is emerging from a slight dip, but never the less remaining positive in the last 12 to 18 months.

Historic Unit Costs show a slight softening over the last 12 months on net balance of respondents with 54% on CAB Members stating increases on a quarterly basis, but this still remains at a high level. Expected Unit Costs show a slight slip, softening with 62% on net balance expecting further increases where CAB Members match that of the wider construction supply chain.

Reinforcing the slight softening in the Historic Unit Costs is shown in the Cost Factors reported by CAB Members. Whilst 46% of members now report raw materials on net balance as an influence on cost, this is down from circa 70% in the previous 12 months. Whilst energy costs have softened slightly the cost emphasis remains high on wages and salaries with 92% reporting to be the most influential cost factor this quarter which has remained high for the last 12 months.

Likely Constraints on Activity Over the Next 12 Months remains squarely on the continued market demand. Capacity also raises it head as a constrain at 23% this quarter, not seen in the past Q3 and Q4 in 2022, suggesting some respondents are already working near to their capacity. Labour availability has softened over the year at now just 8% respondents reporting as a constraint compared to 15% 12 months ago

With 33% of CAB Members reporting an Expected Capacity Utilisation of 33% over the next quarter, which is little change over the last 12 months, suggests that the market has excess capacity for growth in the coming year. CAB Members continue to exceed the Expected Capacity Utilisation of the wider construction supply chain.

CAB Members have changed emphasis on its Labour Force over the last 12 months whilst this quarter sees 17% of net respondents on balance increasing their labour force in the last year, 67% state on net balance that they are seeking to increase their labour force. This is a reversal where 12 months ago 62% had increased their labour force in the previous 12 months. This suggests a decrease in labour force over the last 12 months and an expectation of an increase in labour requirements in the next 12 month.

Labour costs remain a very high cost for both CAB Members and the wider construction supply chain. Over the last two quarters expected labour costs for the year ahead is greater than the past years increases suggesting further pressure on labour costs in the next 12 months across CAB Members and the wider construction industry.

Capital Investment and therefore confidence in the fenestration market across the membership remains high with 75% of respondents stating that they have and continue to, on net balance, invest in plant and machinery. This investment is closely followed by 50% investing in new product development.

Here at CAB we will be keeping our membership informed of market expectations. Why not consider joining the Association and be recognised as being involved in supporting your Industry and helping to shape its future. More information on our website at c-a-b.org.uk